After recent market volatility, Portfolio Manager Uday Cheruvu writes on some ways to get to the bottom of a tech company's true value.

In 2000, when OneTel was the golden child and seemingly a thousand ASX-listed resources ‘prospectors’ were emerging, phoenix-like, as dot.com companies, price to earnings ratios as a valuation tool was criticised.

Instead, as the gifts to investors were handed out at investor presentations, the valuation techniques cited by the CEOs were more likely to be price to revenue, the annual revenue growth rate, or the old favourite – “Technological advancements mean that it’s different this time”. Just don’t mention the words profit or investor returns.

The new tech companies, part of the Technology, Media, Telecom (TMT) boom, were using (burning, some would say) all their cash chasing revenue growth; to get to a critical mass that would mean that in their new sectors they would be the number one provider.

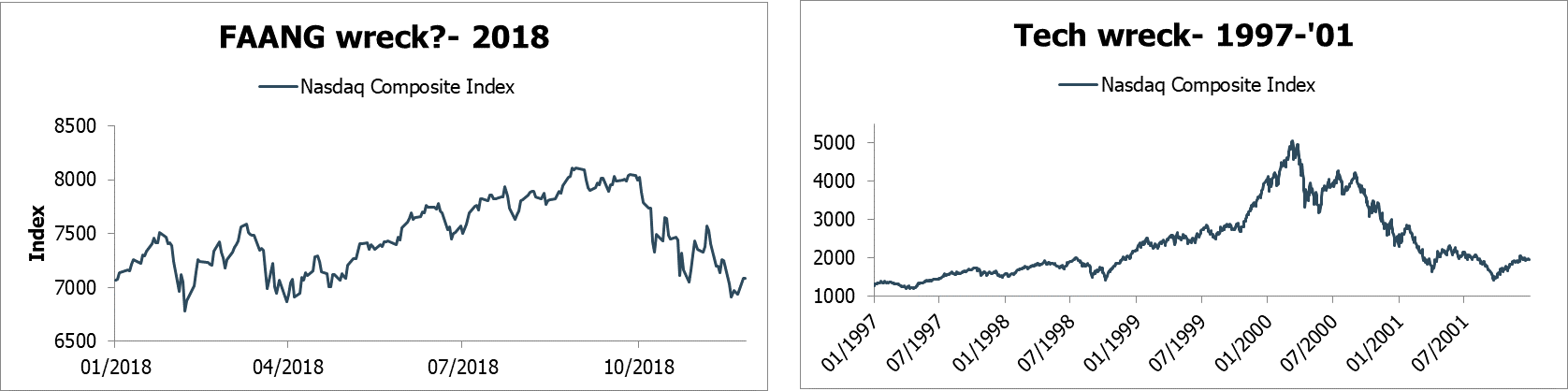

It is interesting to look at the listed tech market in 1999, just as the bubble was deflating. Why is that instructional now? In 2000 venture capital was still relatively easy to come by, the Nasdaq was at a PE of 200 due to a small number of surging stocks, money was relatively cheap but Fed chairman Alan Greenspan was ratcheting up interest rates in an attempt to knock inflation on the head, Japan entered a recession.

In July 2018, venture capital was relatively easy to come by, the Nasdaq was at a significant price to earnings ratio due to a small number of surging stocks, money was still cheap, but Fed chairman Jerome Powell was ratcheting rates. Rumours were that China’s growth would fall substantially, if not enter a recession. You get the idea – there are similarities between the two time periods.

Similarities?

Source: Bloomberg, PM Capital

Price to earnings ratio is one of the more understood valuation techniques so it is used as a valuation technique for most companies. But for most of the tech/ software/ developer stocks you look at, or software developer companies, it's still hard to look at a price-to-earnings multiple. This may be fair, because these companies are not in their normal growth paths but are re-investing heavily into the business rather than producing profits and return on equity.

Alternatively, most people look at a PE to sales basis. Or some sort of other metric that captures the operational worth. Therefore current valuations become secondary to what is the growth potential of these businesses. So if you look at something like a Wisetech (ASX: WTC) or an Afterpay (ASX: APT), why do they trade at such a high valuation? It's because investors are betting that they can create a significant amount of growth and guarantee their position in what is a high growth industry. For example, for FY19 WiseTech has forecast approximately 47% revenue growth to $325m, and EBITDA growth of about 34% to $105 million. On current prices that means its PE is about 100 times. But if it grows by 45% over the next two years, that would bring down the valuation significantly.

The biggest question for investors is over growth sustainability, particularly if a company is priced for perfection. That should be the primary focus when buying these businesses. From our perspective, we think there are some companies which have got underlying growth that are sustainable, while there are question marks over some stocks - if the sharemarket continues to turn, how will they perform in that risk-off environment? Wisetech has a wide remit. It's a high-quality and relatively large company in the data consulting, digital marketing and technology development. Logistics companies around the world still use Excel spreadsheets to do most of their internal analysis and internal work. Wisetech is a sales business that replaces Excel spreadsheets with a front end software system. Now that is a huge market. So how much will it grow by over the long term?

That's the question mark that we've worked hard to glean, given where the valuation is at, but it's hard to argue that it's not a high-quality business.

Source: Bloomberg

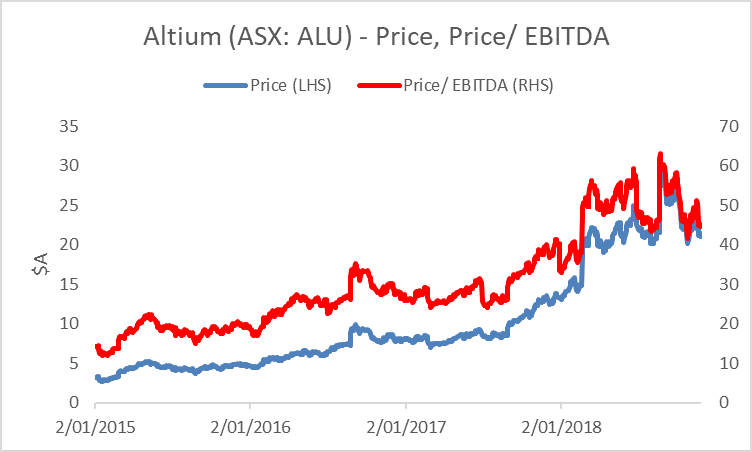

We also like Altium (ASX: ALU), an Australian-domiciled owned public software company that provides PC-based electronics design software for engineers who design printed circuit boards. Unusually for tech companies, it actually has a PE (around 40 times)! Its underlying business is PCB software - basically green boards that all the chips are put on when you buy tech goods. Altium makes the software that people use to design these boards.

Historically they've had a huge piracy problem; they have not been able to get their users to pay them, particularly in China. However, that problem is turning around as piracy is falling the world over. That means they have re a huge growth potential not because their software is penetrating any further, but that people are starting to pay. That sort of a structural change is a positive for their business which I think warrants their valuation.

This article reflects opinions as at the time of writing and may change. PM Capital may now or in the future deal in any security mentioned. It is not investment advice.