Recent news on licence extensions and the easing of China’s COVID-zero policy suggest changing fortunes for the sector heading into 2023.

By Kevin Bertoli, PM Capital

Key Points

- Shares of casino companies with operations in Macau were volatile in 2022 with China’s ongoing COVID-zero policy and the uncertainty surrounding licence renewals acting as negative headwinds.

- However, in November the outlook began to improve after Macau’s Government granted Macau’s six existing casino operators new 10-year licences. China’s recent relaxation of its COVID-zero policy should lead to a recovery in casino patronage.

- PM Capital retains a positive view on Macau’s casino industry due to its long-term growth prospects, favourable market structure and attractive returns.

Introduction

In 2022, Macau’s six gaming operators saw the conclusion of their initial 20-year gaming licences and were awarded new 10-year licences. Although gaming has long been a feature in Macau, a former Portuguese colony which is now part of China, the passing of its Gaming Law (Law 16/2001) in 2001 ushered in two decades of eye-watering growth. Over the 20-year period, Macau’s six concession holders developed 17 integrated casino resorts and generated more than US$36 billion in gaming revenue in 2019, dwarfing even that of Nevada and the Las Vegas Strip.

PM Capital has followed Macau closely over the last two decades and has invested in the market on numerous occasions through the US-listed parent companies of local concessions holders (i.e. Wynn Resorts, Las Vegas Sands) as well as the local concessionaires themselves, which are primarily listed in Hong Kong (i.e. Wynn Macau, Sands China).

PM Capital’s largest holding today is US-listed Wynn Resorts, which owns and operates casinos in Las Vegas, Boston and Macau. Despite its US origins, prior to the pandemic Macau had emerged as Wynn Resorts’ largest earnings contributor at over 70% of adjusted EBITDA. We also hold positions in Sands China and MGM China.

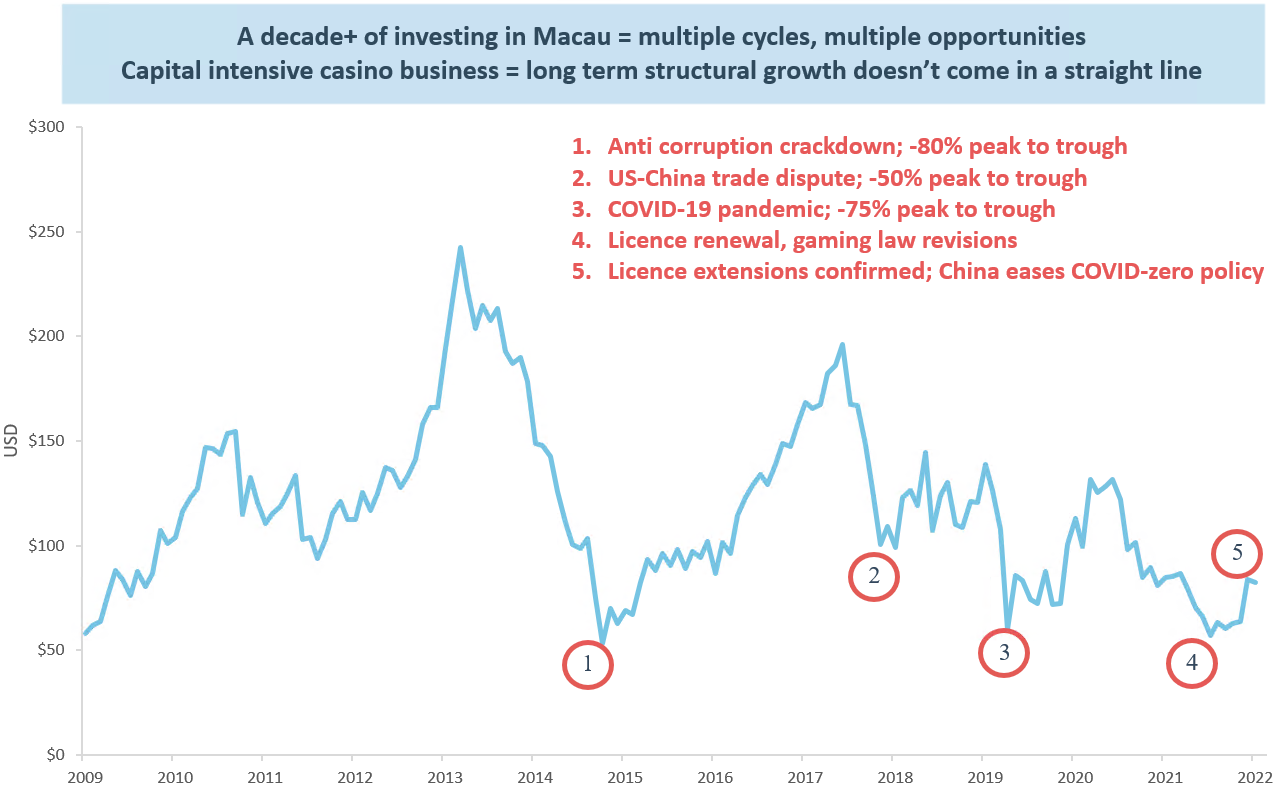

Despite the attractive long-term growth prospects, favourable competitive dynamics and stellar long-term returns, there have been multiple opportunities to invest in the sector. The below chart of Wynn Resorts highlights the volatility experienced by the industry over time, which has provided many opportunities to invest.

Chart 1: Wynn Resorts

Source: Factset

COVID-19, Licence renewals

The last three years have been particularly difficult for Macau with the COVID-19 pandemic causing a significant earnings disruption at the same time as the impending 2022 licence renewals presented another unknown for investors to navigate.

The initial COVID-19 wave in 2020 saw the share prices of casino companies fall anywhere from 50-75% peak-to-trough as governments worldwide placed restrictions on the movement of their citizens and the global economy came to a screaming halt.

Given our long-term focus, PM Capital saw this as an opportunity to add to our gaming positions. At its COVID-19 low, Wynn Resorts traded on a Price Earnings (PE) multiple of less than 5 times its normalised earnings, according to our analysis, with no value being ascribed to Macau operations.

However, while countries around the world emerged from COVID-19 lockdowns, and casino markets like Las Vegas thrived thanks to pent-up consumer demand and stimulus measures, Macau with its reliance on visitation from Mainland China and Hong Kong continued to be severely impacted by China’s COVID-zero strategy, which led to rolling lockdowns and strict movement controls.1

Wynn Resort’s financial performance succinctly highlights the contrasting fortunes of gaming markets globally post pandemic, with its Las Vegas properties achieving adjusted EBITDA levels over 85% higher than its pre-COVID performance while Macau recorded an adjusted EBITDA loss2.

The pandemic also coincided with a once-in-20-year event: licence renewals and the revision of Macau’s Gaming Law. This led to further investor apprehension, particularly towards operators with links to the US who were considered at greater risk of not having their licences extended given the current geopolitical tensions between the US and China.

The impact was most notable in September 2021 when stocks fell 20-40% after the Macau Government published a public consultation document as part of the Gaming Law revision process. This document asked Macau residents to provide feedback on a range of issues and worrisomely raised the prospect of greater regulatory oversight of Macau casinos, introduction of restriction on repatriation of capital from Macau and a desire for an increase in local ownership stakes, causing concern amongst investors.

Although these concerns proved to be largely unfounded – the Government released details of its proposed gaming-law revisions in January 2022 and there would be no dividend restrictions or further government oversight – the issue of licences had yet to be fully resolved and the stop-start nature of China’s COVID-19 elimination policy had delayed the expected earnings recovery for Macau casino operators.

But has Macau finally been dealt a better hand?

Positive news 1: Licence renewals

In November 2022 at a public press conference, Macau Government representatives announced that all six existing casino operators in Macau would be awarded new 10-year licences. This announcement removed one of two key overhangs plaguing the sector. Wynn, Sands and other casino stocks rallied on this news.

Licences were officially signed on December 16 and further detail provided as to the investment commitments made by each operator. The six licence holders will invest a minimum of US$15 billion over the next decade. About 90% of that investment is in non-gaming operations. Wynn Macau (owned by Wynn Resorts) will invest about US$2.2 billion during its 10-year term. Sands China has committed to US$3.8 billion. PM Capital views the level of investment required to extend licences as a positive outcome for operators.

Macau also finalised and reduced the number of satellite casinos in Macau, from 18 to 11. Satellite casinos are administered by authorised operators but owned and managed by third parties. The change slightly reduces competition in Macau.

Positive news 2: COVID-19 policy

In early December 2022, China took a major step towards abandoning its COVID-zero strategy when it eased a range of restrictions. After mounting public pressure, China’s abrupt U-turn in its COVID-19 strategy surprised the market.

COVID-19 case numbers in China are expected to rise as lockdown restrictions ease. But new modelling from global health authorities predicts COVID-19 infections in China will peak in January 2023.3 Cases could begin to fall during the Chinese New Year period (January 22-29), but the market currently has a low expectation of this scenario.

For Macau casinos, capacity restrictions have been removed. Since 2020, gaming floors were limited to half their assessed capacity for guests, casino tables and seats. Now, operators can go back to pre-COVID-19 levels (with a 1-metre distance requirement) with capacity restrictions not posing a limitation when visitation recovers.

Other changes at Macau casinos include:

- A resumption of e-Visa applications for Mainland Chinese citizens

- Restrictive quarantine requirements have been removed for all visitors (international visitors still have to lodge a Rapid Antigen Test on days 1-3)

- Removal of departure restrictions on positive cases in Macau returning to the Chinese mainland. The fear of getting trapped in Macau after contracting COVID-19 was an obstacle to visiting.

- QR codes are no longer mandated

These restrictions are unambiguously good news for Macau casino operators. If China follows the experience of Western countries after lockdowns, Macau casinos could experience sharply higher patronage in 2023 because consumers were starved of entertainment during lockdown and have more disposable income as a result.

Long-term outlook

PM Capital’s positive view on Macau is based on five main factors:

- Clearly defined industry landscape: With licences extended for another 10 years the competitive position of a small group of operators is now well defined. With limited land allocations for each operator there is a low risk of excess capacity emerging - a common occurrence in open markets such as Las Vegas - ensuring the high industry returns are maintained.

- Large addressable mass market opportunity: Historically the lower margin, volatile VIP business has dominated gross gaming revenue in Macau. The VIP business has diminished considerably in recent years and Macau’s future success will be more aligned with growth in China’s emerging middle class. More than half of China’s population has entered the middle class, from an estimated 3% in 2000.4 China knows there is strong demand amongst citizens for casino gaming and that Macau is the best place to contain and regulate it.

- Improving accessibility: Macau is 60 kilometres west of Hong Kong on China’s southwestern coast. While Macau’s key customer has always been ‘just across the border’, access to Macau has not always been easy. Continued improvement in transportation infrastructure and more favourable visa policies coupled with an increase in hotel rooms and non-gaming attractions should encourage tourism growth for years to come.

- World-class casino operators in Macau. Wynn Resorts, Las Vegas Sands and MGM Macau have decades of experience in the gaming, tourism, and leisure sector and are well placed to benefit as Macau develops beyond gaming. The presence of US operators also brings with it a high levels of corporate transparency and a disciplined approach to capital allocation.

- Attractive return on capital invested: Despite having fewer casinos than Las Vegas, Macau generates far more gaming revenue than the world’s most recognised gaming mecca. Most casino properties in Macau have a return on investment (ROI) of 15-20%, and while this is down from stratospheric levels a decade ago, it still compares favourably to a single-digit return for most Las Vegas casino operators.

Conclusion

PM Capital’s investment in Macau casino operators since 2009 highlights how structural industry change does not occur in a straight line. In developing industries, there can be multiple cycles within the trend.

Although casino stocks have rallied on the recent news, in the short term the environment may remain volatile as China deals with the realities of relaxing its COVID-19 restrictions. But we suspect the recovery has further to run over the next few years as China finally emerges from the pandemic and Macau can return to growth.

On PM Capital’s normalised earnings assumptions, Wynn Resorts and Sands China continue to trade at depressed levels. Wynn Resorts and Sands China currently trade between 12-13 times normalised pre-COVID earnings.5 With licence risks now removed as the environment improves, we expect these companies will trade closer to their long-term valuation – a PE closer to 20 times normalised earnings – suggesting material upside from here remains.

About the author

Kevin Bertoli is Co-Portfolio Manager of the PM Capital Global Companies Fund and PM Capital Australian Companies Fund. More PM Capital insights are available here.

1 ~90% of visitors to Macau in 2019 came from Mainland China and Hong Kong. https://dataplus.macaotourism.gov.mo/document/ENG/Book/VAHightlights/2019/tourism%20highlights_Dec_2019_E.pdf

2 Trailing 12 month adjusted EBITDA performance to Sept 2022.

3 CNBC, “New Covid Model Predicts over 1 Million Deaths in China through 2023,”. 17 December 2022. https://www.cnbc.com/2022/12/17/new-covid-model-predicts-over-1-million-deaths-in-china-through-2023.html

4 ChinaPower, (2022), “How well-off is China’s Middle Class”.

5 At 31 December 2022, estimates for Wynn Resorts given no value to the announced UAE project and assumes loss making Interactive division achieves breakeven .

This Insight is issued by PM Capital Limited ABN 69 083 644 731 AFSL 230222 as responsible entity for the PM Capital Global Companies Fund (ARSN 092 434 618) and the PM Capital Australian Companies Fund (ARSN 092 434 467), the "Funds". It contains summary information only to provide an insight into how we make our investment decisions. This information does not constitute advice or a recommendation, and is subject to change without notice. It does not take into account the objectives, financial situation or needs of any investor which should be considered before investing. Investors should consider the Target Market Determinations and the current Product Disclosure Statement (which are available from us), and obtain their own financial advice, prior to making an investment. The PDS explains how the Funds' Net Asset Value are calculated. Past performance is not a reliable guide to future performance and the capital and income of any investment may go down as well as up.