Portfolio Manager Douglas Huey reports on price to revenue valuations in this hot market sector.

Technology continues to be one of the strongest market sectors, but we are clearly at a point where software is a major market theme of its own, and, within that, the evolution of Software-as-a-Service (SaaS). This is software hosted remotely through the cloud, with the software vendor taking care of the underlying infrastructure needs. Atlassian is probably the most well-known SaaS provider in Australia, led by its Jira and Confluence services.

Customers like SaaS because they enjoy lower running costs, up-to-date features, and better security. The SaaS providers can better control the usage of their software, reducing piracy as customers need regular updates that are provided via the web. It will continue to grow strongly for years to come.

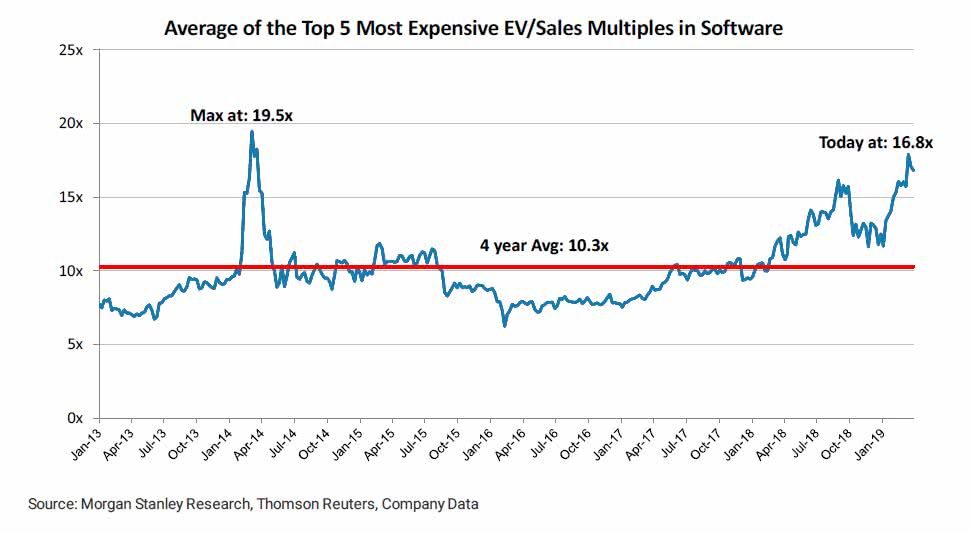

Unsurprisingly, investors love the software stocks. These days, the more interesting fast growing SaaS companies are regularly valued at between 15-20X sales, based on 2018 sales. The market tends to value these companies based on a multiple of sales because, as a rule of thumb, these exciting growth companies are not especially profitable, and therefore a traditional PE ratio valuation is not as relevant. In addition, they are not particularly cash generative, unlike the various established software companies like Microsoft and Oracle.

The cash flow picture is further complicated if we take into account that they commonly use generous stock compensation schemes to reward their staff.

Indicating the power of market positioning, in the US the share prices of the software giants continue to beat the broader sector (but they are also at their recent highs versus sales):

The more things change the more things stay the same. Below is a quote from the former CEO of Sun Microsystems, Scott McNealy after the end of dotcom boom. He commented (with the benefit of hindsight) how inappropriate a valuation based on a revenue multiple was back in the early days of the internet revolution[1]:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

Interesting that at its peak in 2000 Sun hit 10x revenues. Unsurprisingly, the above comments were made in 2002.

Without a doubt, some of these SaaS companies will grow into great businesses in time. My colleague Uday Cheruvu has written about Australian companies Wisetech and Altium (the latter of which actually has a P/E). Inevitably, some will fade away as well as the technology industry is cyclical and only the strong will survive. One wonders if you need to be very careful to value these software companies using multiple of sales despite their rosy growth outlook (for now?). Valuation matters when it comes to making money from stocks. Margin of error when buying small but fast growing companies is low, especially if they are valued highly.

[1] https://finance.yahoo.com/news/what-were-you-thinking-180823527.html:

This article reflects opinions as at the time of writing and may change. PM Capital may now or in the future deal in any security mentioned. It is not investment advice.