Douglas Huey, Portfolio Manager, reports that we have had the equivalent of a bull market in Information Technology (IT) spending.

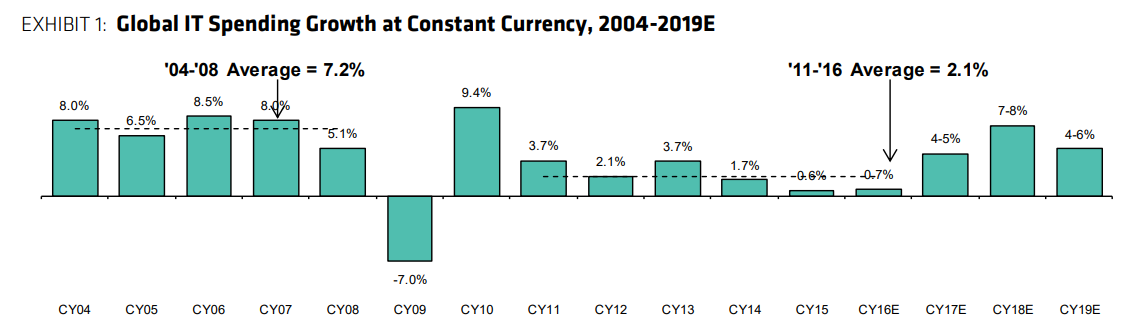

Bernstein Research has been tracking global IT spending over the years and the two most relevant findings for now are that IT spending in 2017 - 2018 was above trend; and that IT spending can be cyclical.

In such an environment, particularly with interest rates close to zero, more companies can grow and prosper in the short term than can be expected to survive in more common trading conditions. The Software as a Service (SaaS) sector has certainly been a beneficiary of the boom, triggering a number of IPOs and pushing “young software” stocks to aggressive enterprise value/ sales ratios of 10-20 times.

The important question is how these SaaS companies will cope if/ when the robust IT spending environment falters (which it looks like it is currently doing) either due to cyclical or structural factors, and clients decide to:

- Do less…: As IT budgets are curtailed, IT departments focus the budget on spending that is critical to keep the business running. Strategic digital transformation projects (so-called) are put on hold.

- …with less, or different: IT departments and subscriptions are cut back. Subscription revenue – an alluring concept for those investing is SaaS as it is regular and non-lumpy – rolls over, with customers paying less if they reduce their workforce. SaaS projects are also much less painful to deploy than traditional enterprise software. Remember the horror stories of massive cost and time over runs? Naturally, it strongly entrenched the software vendor with the customer. It remains to be seen if current SaaS software is as entrenched when someone else comes up with a better/ cheaper mousetrap.

As a long term investor, we are looking for solidly profitable companies trading at a reasonable valuation, with a trustworthy management team.

Just as importantly, it needs to be able to be counted on to grow in good and bad times. Can these companies outrun the bad times?

This one special quality sounds simple but it is actually very difficult to do. History is littered with the gravestones of successful companies that looked to diversify but only succeeded in sucking up valuable capital and management attention from their main business.

The hallmark of a great company is the ability to expand beyond its core business and successfully dominate a new or adjacent opportunity. A few examples:

- Google expanded beyond desktop search and created the Android operating system. Android has since become the dominant mobile eco-system. In a nicely virtuous circle, Google now dominates mobile search as well.

- Oracle has long dominated the database market. Over the years, it has built up its application business and has become the second largest enterprise application vendor. It is now aggressively looking to grow market share as the enterprise application market shifts to the cloud.

- Drawing on the strengths of eBay and Costco, Amazon has become an online retailing behemoth. Remarkably, at the same time it has also managed to invent Amazon Web Services (AWS), the leading cloud computing platform.

- Samsung is another champion that is often overlooked. It is remarkable how Samsung has built up three franchises in its history – memory, mobile phone, and OLED display.

- In the software market, we have Microsoft. It started life in the PC market, supplying the underlying operating system. Over the years, it has expanded its portfolio – Office, SQL Server, NT, and Azure to name a few.

Most of the new generation SaaS companies are focusing on their niches. However, their core markets will mature and growth will slow down as competitors catch up.

Can the current IT stars do the same internal diversification successfully, while still retaining their core markets? Just because a small software company can grow 30-50% for 2-3 years in a robust IT spending environment, there is no guarantee that it can dominate its core segment in the long run, let alone execute the most tricky business strategy of all – building and conquering new market opportunities.

And yet, they are already valued like great companies built for long term success.