Copper supply: recent developments

Supply constraints support our view on copper

By Kevin Bertoli, PM Capital

Key points

- The market’s bearish view on copper for 2024 has weakened, amid the return of production supply disruptions and downgrades.

- Recent legal developments in Panama required First Quantum to suspend production at its Cobre Panama copper mine.

- In addition, key copper producers, such as Anglo American, have downgraded production guidance.

- These supply constraints mean the copper market now looks like being balanced or even in deficit in 2024, against previous market expectations that copper would be in surplus.

Introduction

PM Capital’s favourable view on copper is based primarily on supply constraints. We initiated positions in leading copper producers in 2019, believing copper supply would lag demand during this decade.

We noted falling copper grades across the industry, a lack of new mega-deposit discoveries, and extra time and cost to bring new supply to market as geology became more challenging and environmental permitting more rigorous.

New copper supply would be needed to meet rising demand. Copper is a key material in electric vehicles and other renewable energy systems. But large new copper deposits have become harder and costlier to develop.

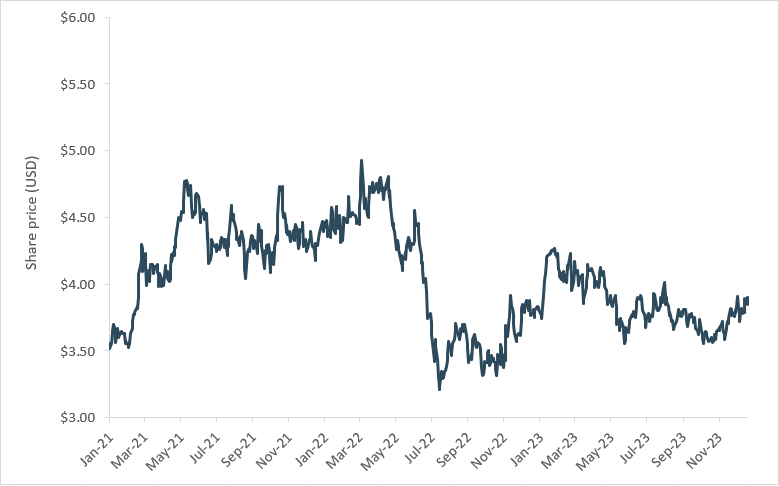

Copper was US$2.50 per pound when PM Capital began to analyse the industry in 2018. Copper was US$3.86 in mid-December 2023, as Chart 1 below shows:

Chart 1: Copper price

Source: Bloomberg

We maintain a positive long-term view on copper this decade, believing supply challenges will create a supply-demand imbalance, supporting a higher copper price. These three developments further confirm that view:

1. Cobre Panama

In late November 2023, the Panama Supreme Court ruled that the terms of the Panama government’s contract with First Quantum Minerals to operate the Cobre Panama mine were unconstitutional.

Cobre Panama is a large, open-pit copper mine, about 120 kilometres west of Panama City and 20 kilometres from the Caribbean Sea coast. The mine commenced production in 2019.

First Quantum, a Canadian company that owns 90% of Cobre Panama, describes Cobre Panama as ‘one of the largest new copper mines opened globally over the past decade’.1 The mine has 3 billion tonnes of proven and problem reserves.2

Cobre Panama has been controversial. The Panama Supreme Court’s decision followed nationwide protests that blocked roads and shipping routes as Panamanians fought back against the mining sector’s expansion there. Opposition to Cobre Panama has been building for years, reinforcing sovereign risk in mining.

First Quantum has had to cease operations at Cobre Panama, which was expected to produce 385,000 tonnes of copper in 2024. That production puts Cobre in the top 10 copper mines globally. Cobre Panama was expected to contribute 1.75% of total global copper supply in 2024.

It is possible that Cobre Panama could remain closed until the Panama election in May 2024, taking a significant amount of production from global copper supply.

2. Anglo American cuts production guidance

In December, Anglo American, a top-10 copper producer, cut production guidance for 2024 by around 195,000 tonnes due to geotechnical problems and challenging ore. That downgrade equates to almost 1% of global copper supply. The news contributed to a sharp fall in Anglo American shares.

BMO Capital Markets, an investment bank, this month said production guidance from a number of copper producers had come in below market expectations.3 That reinforces PM Capital’s view that copper is proving harder to mine.

BMO analysis shows more than 750,000 tonnes of copper – about 3% of global supply has been removed from the market recently due to production guidance downgrades and the Cobre Panama shutdown.

3. From surplus to potential deficit

The market’s previous anticipation of a large surplus in copper supply for 2024 has dissipated. BMO estimates a deficit (copper contained) of 75,000 tonnes of copper next year, from a previous expected surplus of around 200,000 tonnes. Small copper surpluses are expected in 2025 and 2026.

On the demand side, BMO estimates global copper demand to rise 1.8% in 2024, partly due to higher demand from China. However, growth is sub-trend due to weaker expected demand from Europe and the United States.

Conclusion

PM Capital’s copper thesis remains firmly intact. Recent developments support our view that copper faces ongoing supply challenges and disruptions at a time of rising demand this decade.

As is always the case with commodities, there will be periods when copper is in and out favour this decade. But the long-term trend for copper is positive, amid an ongoing commodities supercycle.

About the author

Kevin Bertoli is the co-Portfolio Manager of PM Capital’s Global Companies Fund and Australian Companies Fund. PM Capital is a leading asset manager in Australian and global equities, and interest rate securities. More PM Capital Insights are available here.

Notes

1First Quantum Minerals website. At 19 December 2023. https://www.first-quantum.com/English/our-operations/default.aspx

2ibid

3BMO Capital Markets (2023), “Copper: 2024’s ‘Bad Year’ disappears’. BMO Global Commodities Research. 10 December 2023.

This Insight is issued by PM Capital Limited ABN 69 083 644 731 AFSL 230222 as responsible entity for the PM Capital Global Companies Fund (ARSN 092 434 618), the "Fund". It contains summary information only to provide an insight into how we make our investment decisions. This information does not constitute advice or a recommendation, and is subject to change without notice. It does not take into account the objectives, financial situation or needs of any investor which should be considered before investing. Investors should consider the Target Market Determinations and the current Product Disclosure Statement (which are available from us), and obtain their own financial advice, prior to making an investment. The PDS explains how the Fund's Net Asset Value are calculated. Past performance is not a reliable guide to future performance and the capital and income of any investment may go down as well as up.