High levels of equity market volatility are currently rarer, but that does not mean that the movements cannot be alarming.

We have become so accustomed to relatively low general levels of volatility, even off a small base, that when we get the significant price action such as that of December last year when the market pulled back significantly over a period of weeks, or in response to adverse individual market events such as a setback in trade talks, that there are concerns of a major short term meltdown.

However, consider these kinds of retractions in the light of history: December’s -4.2% performance (MSCI World Net Index (AUD)) versus, for example, the volatility in the early/ mid decades of the 20th century, where 12 of the 20 largest daily percentage losses occurred in or soon after the Great Crash of 1929[1]).

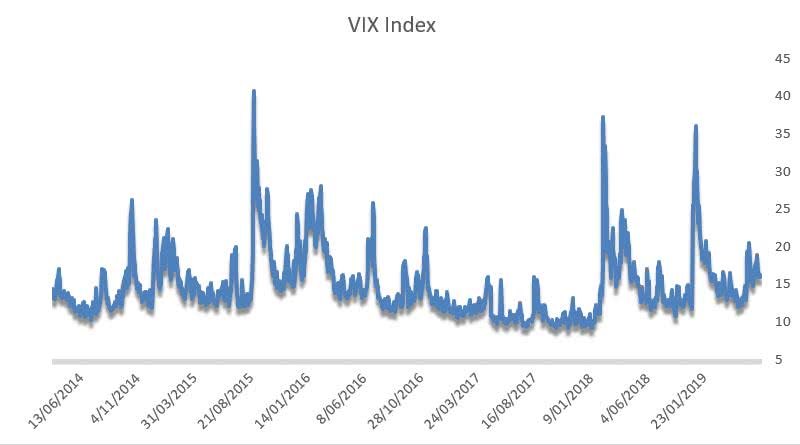

The fear index - VIX

The US VIX Index is a popular tracker of market expectations of volatility for the S&P 500. It is known as the ‘fear index’, so when increased longer-term volatility reflected in the VIX comes the headlines are likely to be inflammatory, for example, ones that go something along the lines of “Volatility fears up 25%!”. However, such headlines are simply playing on the low base that has been baked into the index by several years of below average volatility thanks to rising earnings and the most accommodative monetary policy since (arguably) forever.

As at the time of writing the Vix is trading at about 15 and for most of 2019 it has been trading below 16. In contrast, since January 1990 its average has been approximately 19.3. Even if it returns to its average, that will equate to a 22% move in the index. The chart will be frightening – as individual day spikes above, but its direct relevance to market conditions less so.

As an equities manager we are not averse to volatility. In fact, we can welcome it because it can shake loose opportunities to pick up mispriced companies. Some of the companies that we’ve been watching are back to their highs, despite the losses of late 2018 and scares in 2019 (e.g. via trade disputes). Has there been a change in these companies’ fundamentals, or are they being dragged along by the weight of investors who seem ready to accept it will remain a relatively sanguine market environment?

Concentrating on organic earnings growth is the order of the day.

Would you like more insights? Subscribe below!

More on the Global Companies Fund

More on the ASX-traded Global Opportunities Fund

This article reflects opinions as at the time of writing and may change. PM Capital may now or in the future deal in any security mentioned. It is not investment advice.

[1] Stockcharts.com